Vertical Skew is the shape of the implied volatility (IV) term structure for a single options chain maturity. There is also something called a horizontal skew which is the IV across maturities. The movement of the vertical skew structure has been of interest to me recently when analyzing some of my option positions.

I had a long put butterfly position on with center short strikes 20 points below market. At trade initiation my greeks were as follows: Delta: -56, Gamma: -1.04, Theta: 117.9, Vega -343.8. This is generally what you’d expect for a short vol position. Delta is slightly negative due to the fly being bearishly positioned. My expectation was that for any decline in the markets you’d expect reduced pnl decline due to the fact that the delta will partially offset vega. As it turns out this is not the case, my position actually gained money on a price decline which was opposite to what my greeks are telling me. To understand we must look at IV Skew.

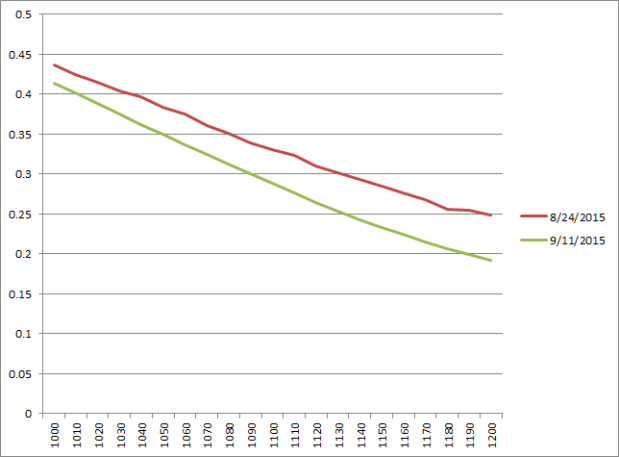

Below are the IVs for RUT September 2015 expiration put options. I specifically picked this period to illustrate the transition from high vol to low vol environment. If you look closely, you will notice that the green line is steeper than the red line. The second graph is the difference between the two line – its increasing. As we go from OTM options to ITM options, the rate of change of IV increases. Another words in our graph, ITM options (right side) will decline more in value (steepens) then OTM and ATM option when IV drops (vice versa for increases in IV – flatten). This phenomenon is not captured by the Black Scholes model as it assumes fixed volatility during the lifetime of the option.

Now how does this help me understand what happened to my position? Well, my right wing (highest strike) put option within my fly is an ITM option. When I was analyzing my position, I assumed that the long put wings of my fly had equal pnl contribution but that’s not the case. My right wing benefited the most from a given IV increase which means the overall negative effect of vega was over-estimated. In fact it may (and I am not 100% sure) be that both delta and vega was working in my favor assuming that the pnl contribution of the long wings was greater than the losses incurred from the short center strikes of my fly. Armed with this information, I think people can incorporate this in to their adjustments and maybe create some ways to exploit this. Open to any ideas!

Pretty cool eh?

Glad to see you back! With Michael Kapler not posting much recently, your work helps fill the gap!